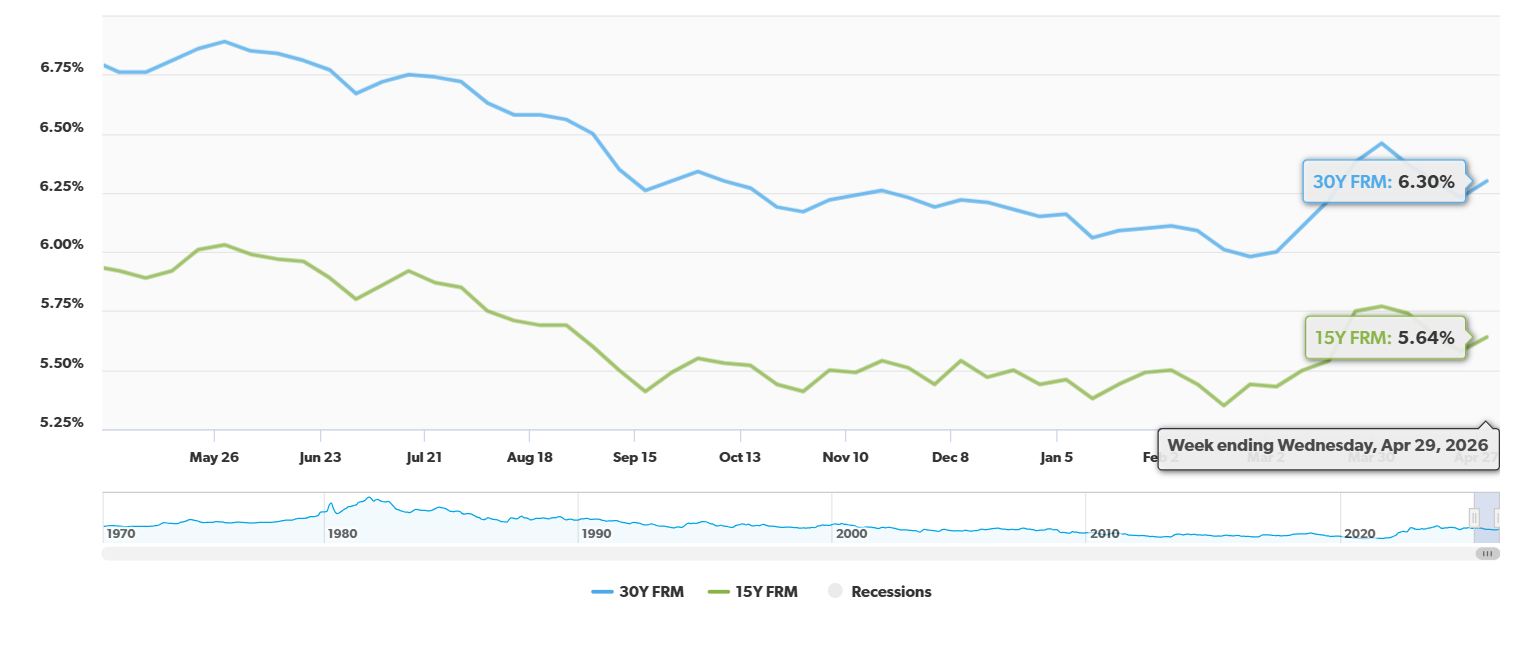

The average rate for a 30-year fixed mortgage has climbed back up to 6.30%, according to the latest Freddie Mac Primary Mortgage Market Survey (PMMS). This modest increase puts an end to a three-week stretch where rates had been steadily declining, signaling a potential shift in the housing market’s immediate trajectory and impacting affordability for many hopeful homebuyers.

30-Year Fixed Mortgage Rate Rises Ending 3 Weeks of Steep Decline

It’s been an interesting few weeks watching the mortgage rate roller coaster. Just when we thought things were cooling off and rates were settling into a comfortable downward trend, they’ve decided to take a little jump upwards. I find these shifts fascinating because they don’t just happen in a vacuum. There are real economic forces at play, and these changes ripple out to affect real people trying to achieve the dream of homeownership.

When I last checked in, the rates for a 30-year fixed mortgage had been inching down. This was great news for potential buyers because it meant their monthly payments could potentially be lower, and they might be able to afford a bit more house. But as you’ll see, the market can be a bit of a fickle friend.

What the Numbers Tell Us This Week

Let’s break down what Freddie Mac, a trusted source for mortgage rate data, reported this week.

- 30-Year Fixed-Rate Mortgage: The average rate is now 6.30%. This is up from 6.23% last week.

- 15-Year Fixed-Rate Mortgage: This type of mortgage, often chosen by those looking to pay off their homes faster or refinance, also saw a slight increase to 5.64%, up from 5.58% last week.

It’s important to put this into a longer perspective. While this week’s bump is noticeable, the overall picture is still more favorable than it was a year ago.

A Year-Over-Year Comparison: A Ray of Hope?

| Mortgage Type | Current Rate (as of 05/01/2026) | Rate Last Week (as of 04/24/2026) | Rate Last Year (as of 05/01/2025) | Weekly Change | Yearly Change |

|---|---|---|---|---|---|

| 30-Year Fixed | 6.30% | 6.23% | 6.76% | +0.07% | -0.46% |

| 15-Year Fixed | 5.64% | 5.58% | 5.92% | +0.06% | -0.28% |

What does this yearly difference mean for a borrower? Let’s imagine you’re buying a $400,000 home.

- At 6.76% (a year ago): Your principal and interest payment would be roughly $2,595 per month.

- At 6.30% (this week): Your principal and interest payment would be roughly $2,472 per month.

That’s a difference of about $123 per month in your favor, or nearly $1,500 saved annually, just on the loan itself. This might not seem like a massive amount to some, but over the 30 years of a mortgage, it adds up to tens of thousands of dollars. It can be the difference between affording a home or not.

Why the Reversal? Delving Deeper

So, what’s causing this slight uptick after a period of decline? The Chief Economist at Freddie Mac, Sam Khater, offered some insightful commentary. He pointed out that purchase applications have actually been rising – up by over 20% compared to the same time last year. This surge, he suggests, is a direct result of buyers responding to the previously lower rates and an increased inventory of homes available. It’s a classic supply and demand scenario playing out in the housing market.

However, we can’t ignore the broader economic forces. My own take is that this week’s movement is a gentle reminder from the financial markets that they are paying close attention to inflation. Recent data, particularly concerning core Personal Consumption Expenditures (PCE), has shown that inflation isn’t quite as subdued as some might have hoped. When inflation shows signs of stubbornness, it can lead to speculation that interest rates might need to stay higher for longer, or even see small increases, to keep things in check. This uncertainty often translates into mortgage rates.

Think of it like this: when the economy is running a little too hot, the Federal Reserve (and by extension, mortgage rates) acts like a thermostat. If things are heating up (inflation), they might turn the temperature up a notch to cool it down. This week’s rate rise could be a small adjustment in response to those inflation signals.

The Buyer’s Reaction: A Balancing Act

It’s a balancing act for buyers right now. On one hand, the rates are still lower than last year, which is a significant advantage. On the other hand, this recent uptick means that the savings gained from the previous weeks’ declines might be slightly diminished for new applicants.

I’ve spoken with many aspiring homeowners lately, and the sentiment is often one of cautious optimism. They were excited by the declining rates, seeing it as their window of opportunity. Now, it’s about re-evaluating their budgets and seeing if this new rate still fits.

Here’s what I believe is crucial for buyers to consider:

- Don’t panic: A 0.07% increase might seem daunting, but it’s a small movement in the grand scheme of things.

- Focus on the annually lower rates: You’re still in a better position than you were a year ago.

- Inventory is key: As Sam Khater mentioned, more homes are available. This gives buyers more choices and potentially more negotiating power, which can offset a slight rise in interest rates.

- Get pre-approved: Knowing exactly what you can afford based on current rates is vital.

What’s Next?

Predicting mortgage rates is a bit like trying to predict the weather – you can make educated guesses, but there are always unexpected shifts. The sustained presence of inflation concerns, coupled with the Federal Reserve’s watchful eye, will likely keep mortgage rates somewhat sensitive to economic news.

For now, the 30-year fixed mortgage rate at 6.30% represents the current cost of borrowing for a home. It’s a reminder that the market is dynamic, and staying informed is the best strategy for anyone looking to buy. I’ll be keeping a close eye on the upcoming economic data and Freddie Mac’s surveys to see if this rate rise is a brief pause or the start of a new trend.

🏡 Two Performing Rentals With Strong Cash Flow

Pleasant Grove, AL

🏠 Property: 6th Avenue

🛏️ Beds/Baths: 3 Bed • 2.5 Bath • 1549 sqft

💰 Price: $270,000 | Rent: $1,900

📊 Cap Rate: 6.7% | NOI: $1,514

📅 Year Built: 2026

📐 Price/Sq Ft: $175

🏙️ Neighborhood: B+

Rincon, GA

🏠 Property: Founders Dr

🛏️ Beds/Baths: 3 Bed • 2 Bath • 1600 sqft

💰 Price: $275,000 | Rent: $2,200

📊 Cap Rate: 7.0% | NOI: $1,613

📅 Year Built: 2025

📐 Price/Sq Ft: $172

🏙️ Neighborhood: B+

Alabama’s new build with solid cap rate vs Georgia’s affordable rental with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Build Passive Income & Wealth with Turnkey Rentals

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

🔥 HOT INVESTMENT Properties JUST ADDED! 🔥

Request a Callback / Fill Out the Form Online