If you’ve been dreaming of buying a home or even refinancing your current mortgage, this is fantastic news! The 30‑year fixed mortgage rate has just experienced a significant drop, reaching its lowest point this week in what feels like forever. As of April 23, 2026, this crucial rate now stands at a promising 6.23%, a level we haven’t seen during the spring homebuying season in the last three years. This dip isn’t just a small blip; it’s a signal that the housing market might be regaining some much-needed momentum, making homeownership more accessible for many.

30-Year Fixed Mortgage Rate Drops Steeply to Lowest Level This Week

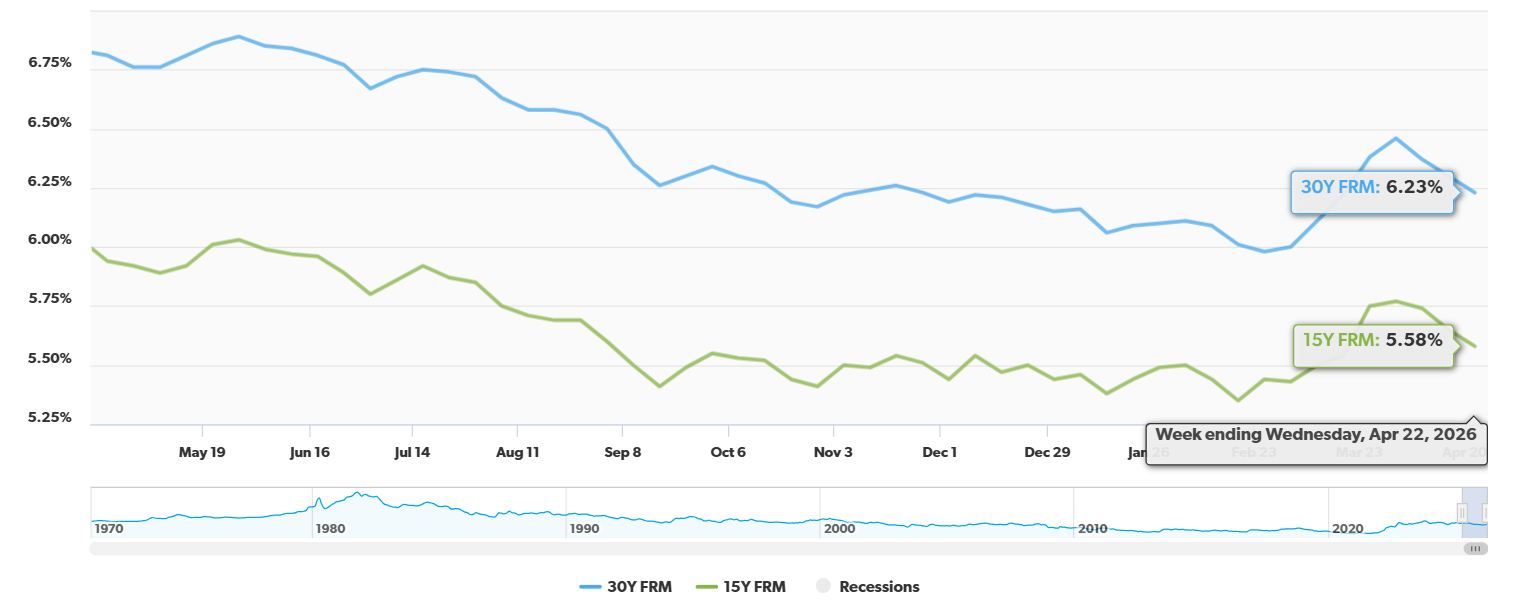

A Significant Shift: Rates Are Down, Way Down

The numbers from Freddie Mac, a key player in the mortgage market, paint a clear picture. For the week ending April 23, 2026, the average 30-year fixed-rate mortgage settled at 6.23%. This is a noticeable decrease from the 6.30% we saw just last week. But the real story is when you look back a bit further. A year ago, this same rate hovered around a much higher 6.81%. That difference is substantial and translates into real savings for borrowers.

It’s not just the popular 30-year mortgage that’s seeing improvement. The 15-year fixed-rate mortgage also declined, now averaging 5.58%, down from 5.65% last week. A year ago, this shorter-term option was at 5.94%.

Understanding the Decline: What’s Behind the Drop?

So, why are we seeing such a steep decline in mortgage rates? A significant factor, according to Chief Economist Sam Khater of Freddie Mac, is the Federal Reserve’s move to lower the federal funds rate. This key interest rate influences borrowing costs across the economy. By lowering it to a target range of 3.50% to 3.75% in late 2025, the Fed has set the stage for mortgage rates to follow suit. When it’s cheaper for banks to borrow money, they can afford to offer better rates to consumers.

This downward trend isn’t an overnight phenomenon. It’s a continuation of a pattern that began to emerge in late 2025. This sustained decline is what gives the current drop its real significance. It suggests a more fundamental shift rather than a temporary fluctuation.

Impact on Homebuyers and Refinancers: What Does This Mean for You?

This drop in mortgage rates has a direct and positive impact on anyone looking to buy a home or refinance their existing mortgage. Let’s break down how.

Potential Savings:

To illustrate the impact, let’s consider the potential savings on a hypothetical mortgage. Imagine you’re looking at a $300,000 mortgage.

| Mortgage Term | Rate This Week (April 23, 2026) | Rate Last Week | Rate Last Year (April 23, 2025) | Approximate Monthly Savings (vs. Last Week) | Approximate Annual Savings (vs. Last Week) | Approximate Monthly Savings (vs. Last Year) | Approximate Annual Savings (vs. Last Year) |

|---|---|---|---|---|---|---|---|

| 30-Year Fixed | 6.23% | 6.30% | 6.81% | ~$100 | ~$1,200 | ~$325 | ~$3,900 |

| 15-Year Fixed | 5.58% | 5.65% | 5.94% | ~$50 | ~$600 | ~$150 | ~$1,800 |

Note: These savings are estimates based on common mortgage calculators for a $300,000 loan amount and do not include taxes, insurance, or other fees. Actual savings will vary.

As you can see, even a small percentage drop can add up to significant savings over the life of a loan. For a 30-year mortgage, saving over $300 a month compared to last year could mean paying off your home faster or having more money for other financial goals.

Increased Buying Power:

For potential homebuyers, lower rates mean you can afford more house for the same monthly payment. This could allow you to:

- Qualify for a larger loan amount: This might mean looking at homes in areas you previously thought were out of reach.

- Lower your monthly payments: If you were already pre-approved, your monthly mortgage payment could decrease, giving you more breathing room in your budget.

- Save money on interest: Over the 30 years of your loan, the total interest paid will be considerably less.

Refinancing Opportunities:

If you currently have a mortgage with a rate higher than 6.23%, now might be the perfect time to consider refinancing. Refinancing can help you:

- Lower your monthly payment: This can free up cash flow for other expenses or investments.

- Reduce the total interest paid: By refinancing into a lower rate, you’ll pay less interest over the remaining life of your loan.

- Shorten your loan term: You might be able to refinance into a shorter term, like a 15-year mortgage, and pay off your home faster, while still potentially saving on your monthly payment compared to your current situation.

Market Momentum: Signs of Life in the Housing Sector

The good news doesn’t stop with just falling rates. Freddie Mac’s report also indicates a pickup in purchase applications, which means more people are actively looking to buy homes. Additionally, there’s been an increase in refinance activity, showing that homeowners are taking advantage of the lower borrowing costs. We’re also seeing an increase in monthly pending home sales, which is a strong indicator of future sales activity.

This combination of lower rates, more applications, and increased pending sales suggests that the housing market is experiencing some positive momentum. After a period of uncertainty, this is a welcome sign for both buyers and sellers. It signifies a more stable and potentially growing market.

My Thoughts as an Observer

In my opinion, this 30-year fixed mortgage rate drop is a significant development we shouldn’t ignore. For a long time, we’ve seen rates climb, making affordability a major concern for many. Seeing them now at their lowest point in recent spring seasons is extremely encouraging. It’s a testament to the fact that the market does, indeed, react to economic shifts, particularly when the Federal Reserve takes action to influence borrowing costs.

I believe this trend is likely to invigorate the housing market. It’s a powerful incentive for those who have been on the sidelines, waiting for a more favorable borrowing environment. The fact that both purchase and refinance applications are picking up reinforces this idea. People are recognizing a good opportunity when they see it.

It’s also important to remember that mortgage rates are influenced by a complex interplay of factors, including inflation, economic growth, and government policy. While the Fed’s actions are a major driver, other economic indicators will continue to shape future rate movements.

🏡 Two Performing Rentals With Strong Cash Flow

Pleasant Grove, AL

🏠 Property: 6th Avenue

🛏️ Beds/Baths: 3 Bed • 2.5 Bath • 1549 sqft

💰 Price: $270,000 | Rent: $1,900

📊 Cap Rate: 6.7% | NOI: $1,514

📅 Year Built: 2026

📐 Price/Sq Ft: $175

🏙️ Neighborhood: B+

Rincon, GA

🏠 Property: Founders Dr

🛏️ Beds/Baths: 3 Bed • 2 Bath • 1600 sqft

💰 Price: $275,000 | Rent: $2,200

📊 Cap Rate: 7.0% | NOI: $1,613

📅 Year Built: 2025

📐 Price/Sq Ft: $172

🏙️ Neighborhood: B+

Alabama’s new build with solid cap rate vs Georgia’s affordable rental with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Build Passive Income & Wealth with Turnkey Rentals

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

🔥 HOT INVESTMENT Properties JUST ADDED! 🔥

Request a Callback / Fill Out the Form Online